The United States has taken a significant step toward resolving long-standing uncertainty in digital asset regulation. On March 17, the U.S. Securities and Exchange Commission and the Commodity Futures Trading Commission issued a joint interpretive framework clarifying how federal securities and commodities laws apply to cryptocurrencies.

The guidance states that most crypto assets are not securities and formally identifies 16 widely traded tokens, including Bitcoin and Ethereum, as “digital commodities.” The move provides a clearer regulatory baseline for exchanges, investors, and developers operating in the U.S. market.

Key Points:

- U.S. regulators classify most major cryptocurrencies as non-securities, reducing legal uncertainty

- A five-part taxonomy defines digital commodities, stablecoins, tools, collectibles, and securities

- Core activities such as staking, mining, and airdrops receive clearer treatment under existing law

- Institutional participation may expand, though legislation is still pending in Congress

A Coordinated Regulatory Shift

The joint interpretation represents a departure from years of case-by-case enforcement. Instead of relying primarily on litigation to define the status of digital assets, regulators have outlined a structured framework grounded in existing law.

The document applies the longstanding Howey test, which determines whether an asset qualifies as an investment contract, across a range of crypto use cases.

In practical terms, regulators distinguish between how a token is initially distributed and how it functions once a network becomes operational and decentralized.

Put simply, a token sale may fall under securities law, while the asset itself can later operate as a commodity or utility within a network.

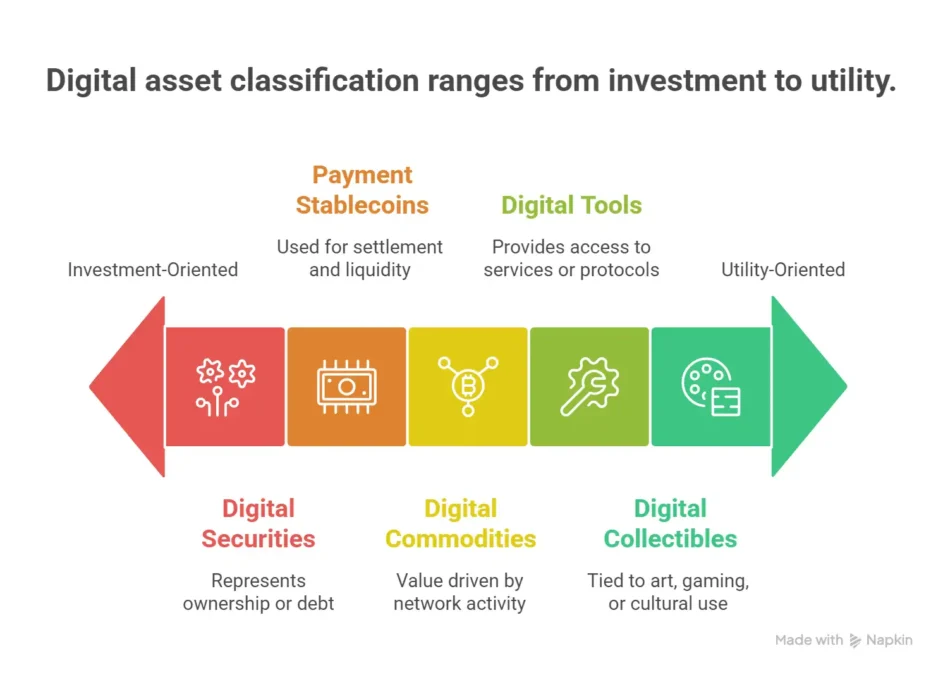

How the Classification Framework Works

The framework introduces a functional taxonomy that groups digital assets based on their economic characteristics and usage.

Digital Commodities

Assets such as Bitcoin (BTC), Ethereum (ETH), and other large-cap tokens qualify when their value is driven by decentralized network activity rather than managerial promises.

Payment Stablecoins

Fiat-referenced tokens used for settlement and liquidity are treated separately, with regulators signaling alignment toward payment or banking oversight rather than securities regulation.

Digital Tools

Utility-based tokens that provide access to services or protocols fall outside securities definitions when no investment-contract characteristics are present.

Digital Collectibles

Non-fungible tokens tied to art, gaming, or cultural use cases are generally excluded from securities treatment unless structured with profit expectations.

Digital Securities

Tokens that represent equity, debt, or explicit profit-sharing arrangements remain under SEC jurisdiction.

Regulators note that classification is not static. Assets may shift categories over time as networks evolve and decentralization increases.

Sixteen Tokens Identified as Digital Commodities

A central feature of the guidance is the explicit identification of 16 crypto assets as digital commodities under federal law.

These include:

- Bitcoin (BTC), Ethereum (ETH)

- Solana (SOL), XRP, Cardano (ADA), Avalanche (AVAX)

- Dogecoin (DOGE), Litecoin (LTC)

Additional assets cited in market summaries reflect similar characteristics, including broad distribution, deep liquidity, and open-source development.

This designation significantly reduces the likelihood that these tokens will be treated as securities in secondary market trading.

Implications for Exchanges and Market Structure

For trading platforms, the framework provides clearer boundaries between securities and commodity markets.

Exchanges listing digital commodities are more likely to fall under a commodities-based oversight model focused on market integrity and anti-manipulation standards. By contrast, platforms facilitating trading in digital securities must comply with securities exchange or alternative trading system requirements.

This distinction allows exchanges to refine listing policies, reduce regulatory risk, and expand product offerings tied to commodity-classified assets.

Clarifying Staking, Airdrops, and Network Activity

The interpretation also addresses several operational areas that have faced regulatory ambiguity.

Protocol-level staking, where participants validate transactions directly on decentralized networks, is generally not treated as a securities transaction when rewards arise from automated network rules rather than managerial efforts.

Similarly, mining activities on proof-of-work networks are not classified as investment contracts, as rewards are linked to computational contribution.

Airdrops are evaluated based on whether recipients provide consideration. In cases where tokens are distributed without payment, they are less likely to meet the criteria for securities offerings.

Wrapped assets, tokens representing underlying crypto on different networks—remain outside securities classification when they maintain a one-to-one structure without additional financial rights.

Market Response and Sentiment

Market reaction to the announcement has been measured. Major cryptocurrencies saw modest gains following the release, reflecting reduced regulatory risk rather than a fundamental shift in macro conditions.

Bitcoin traded within a narrow range below recent highs, while large-cap altcoins experienced selective inflows. Analysts describe the move as a structural development that may influence long-term capital allocation rather than immediate price direction.

Limits of the Framework and Legislative Outlook

Despite its significance, the interpretation does not carry the force of statutory law. Comprehensive digital asset legislation remains under consideration in the U.S. Congress.

Lawmakers are currently reviewing proposals that would formalize jurisdiction between the SEC and CFTC and establish a dedicated regulatory regime for digital assets.

Until such legislation is enacted, the framework serves as authoritative guidance but may evolve through future rulemaking or enforcement actions.

Why This Matters

The joint SEC–CFTC framework provides a clearer regulatory foundation for major crypto assets, reducing uncertainty for market participants while establishing more defined boundaries for compliance and innovation.

What This Means for Traders

- Major assets such as BTC and ETH now carry reduced classification risk in U.S. markets

- Exchanges are likely to prioritize commodity-classified tokens in listings and product expansion

- Institutional participation may increase as regulatory clarity improves

- Smaller or centralized tokens may face heightened scrutiny under securities law

Conclusion

The SEC and CFTC have introduced a more coherent approach to digital asset classification, addressing a core uncertainty that has shaped the industry for years. By distinguishing between securities and commodity-like tokens, regulators have outlined a clearer path for market development.

While legislative finalization remains pending, the direction of U.S. crypto policy is now more defined than at any point in the past decade.

Disclaimer: The information provided in this article is for informational purposes only and does not constitute investment advice. Always do your own research before making financial decisions. Follow us for more updates from coinspectra.in